Removing a Family Member on Health Insurance Marketplace

| | This commodity needs to be updated. (Baronial 2016) |

In the Us, wellness insurance marketplaces,[i] too called health exchanges, are organizations in each state through which people can purchase health insurance. People tin purchase health insurance that complies with the Patient Protection and Affordable Care Act (ACA, known colloquially as "Obamacare") at ACA health exchanges, where they tin can cull from a range of regime-regulated and standardized health care plans offered by the insurers participating in the exchange.

ACA health exchanges were fully certified and operational by January one, 2014, nether federal law.[2] Enrollment in the marketplaces started on October one, 2013, and continued for six months. Every bit of April 19, 2014,[update] 8.02 million people had signed upwardly through the wellness insurance marketplaces. An boosted iv.8 1000000 joined Medicaid.[3] Enrollment for 2015 began on November xv, 2014 and concluded on Dec 15, 2014.[4] Equally of Apr xiv, 2020, 11.41 million people had signed up through the wellness insurance marketplaces.[v]

Private not-ACA health care exchanges also be in many states, responsible for enrolling three million people.[half dozen] These exchanges predate the Affordable Care Act and facilitate insurance plans for employees of minor and medium size businesses.

Groundwork [edit]

Wellness insurance exchanges in the United States aggrandize insurance coverage while allowing insurers to compete in price-efficient ways and help them to comply with consumer protection laws. Exchanges are not themselves insurers, so they do not bear risk themselves, only they exercise determine which insurance companies participate in the exchange. An ideal commutation promotes insurance transparency and accountability, facilitates increased enrollment and delivery of subsidies, and helps spread risk to ensure that the costs associated with expensive medical treatments are shared more broadly beyond large groups of people, rather than spread beyond just a few beneficiaries. Health insurance exchanges utilise electronic information interchange (EDI) to transmit required information betwixt the exchanges and carriers (trading partners), in detail the 834 transaction for enrollment information and the 820 transaction for premium payment.[7] [ better source needed ]

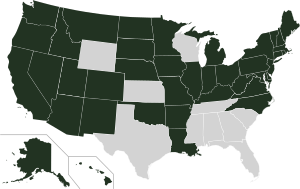

History [edit]

Health insurance exchanges by state.[8] [9] [ needs update ]

Creating state-operated exchanges

Establishing country-federal partnership exchanges

Defaulting to federal exchange

Health exchanges kickoff emerged in the private sector in the early on 1980s, and they used calculator networking to integrate claims management, eligibility verification, and inter-carrier payments. These became pop in some regions as a style for pocket-size and medium-sized businesses to pool their purchasing power into larger groups, reducing toll. An additional advantage was the ability of pocket-size businesses to offer a range of plans to employees, assuasive them to compete with larger corporations. The largest such commutation prior to the ACA is CaliforniaChoice, established in 1996. By 2000, CaliforniaChoice'southward membership included 140,000 individuals from 9000 business organization groups.

Obamacare maintained the concept of health insurance exchanges equally a cardinal component of health care. President Obama stated that it should exist "a market where Americans tin can one-terminate shop for a health care plan, compare benefits and prices, and cull the plan that'southward all-time for them, in the same way that Members of Congress and their families can. None of these plans should deny coverage on the basis of a preexisting condition, and all of these plans should include an affordable basic do good package that includes prevention, and protection against catastrophic costs. I strongly believe that Americans should take the choice of a public wellness insurance option operating alongside private plans. This volition give them a better range of choices, make the health care market more competitive, and keep insurance companies honest."[10] Although the House of Representatives had sought a unmarried national exchange every bit well equally a public option, the Patient Protection and Affordable Care Act (ACA) equally passed used country-based exchanges, and the public option was ultimately dropped from the bill after it did non win delay-proof support in the Senate.[11] States may choose to join together to run multi-state exchanges, or they may opt out of running their ain exchange, in which case the federal regime will step in to create an exchange for utilize past their citizens.[11]

ACA was signed into police on March 23, 2010. The law required that wellness insurance exchanges embark operation in every state on October one, 2013.[12] [thirteen] In the first yr of performance, open enrollment on the exchanges ran from October 1, 2013, to March 31, 2014, and insurance plans purchased by December 15, 2013, began coverage on January i, 2014.[14] [15] [16] [17] For 2015 open enrollment began on November 15, 2014 and ended on February xv, 2015.[xviii] [19] [20]

Implementation of the private exchanges changed the exercise of insuring individuals. The expansion of this market was a major focus of ACA.[21] Over i.3 million people had selected plans for 2015 marketplace coverage in the first three weeks of the year's open enrollment menstruation, including people who renewed their coverage and new customers.[22]

Equally of January iii, 2014, ii meg people had selected a health program through the wellness insurance marketplaces.[23] By April 19, 2014, 8.0 million people had signed up through the wellness insurance marketplaces and an additional 4.viii million joined Medicaid.[iii] As of February, 2015, about 11.4 meg people had signed up for or been automatically renewed for 2015 marketplace coverage.[24] Today, more 1,400 local outreach events have been conducted in federally facilitated marketplace states across the land.[22]

Patient Protection and Affordable Care Act regulations [edit]

- Insurers are prohibited from discriminating against or charging higher rates for whatsoever individual based on pre-existing medical conditions or gender.[25]

- Insurers are prohibited from establishing almanac spending caps of dollar amounts on essential health benefits.[26]

- All private health insurance plans offered in the Marketplace must offer the following essential wellness benefits: ambulatory care, emergency services, hospitalization (such equally surgery), motherhood and newborn care, mental health and substance abuse services, prescription drugs, rehabilitative and habilitative services (services to help people with injuries, disabilities, or chronic weather condition to recover), laboratory services, preventive and health services, and pediatric services.[27]

- Under the individual mandate provision (sometimes chosen a "shared responsibility requirement" or "mandatory minimum coverage requirement"),[28] individuals who are not covered by an acceptable health insurance policy volition be charged an annual tax penalisation of $95, or up to 1% of income over the filing minimum,[29] whichever is greater; this will ascent to a minimum of $695 ($2,085 for families),[30] or 2.5% of income over the filing minimum,[29] by 2016.[31] [32] The penalisation is prorated, meaning that if a person or family unit has coverage for part of the year they won't exist liable if they lack coverage for less than a iii-month period during the twelvemonth.[33] Exemptions are permitted for religious reasons, for members of health care sharing ministries, or for those for whom the least expensive policy would exceed eight% of their income.[34] Also exempted are U.S. citizens who qualify equally residents of a foreign country under the IRS foreign earned income exclusion rule.[35] In 2010, the Commissioner speculated that insurance providers would supply a course confirming essential coverage to both individuals and the IRS; individuals would attach this grade to their Federal tax return. Those who aren't covered will be assessed the penalty on their Federal taxation return. In the wording of the law, a taxpayer who fails to pay the punishment "shall not be subject area to any criminal prosecution or penalty" and cannot accept liens or levies placed on their holding, but the IRS will exist able to withhold time to come tax refunds from them.[36]

| Persons in Family Unit | 48 Contiguous States and D.C. | Alaska | Hawaii |

|---|---|---|---|

| 1 | $11,490 | $14,350 | $xiii,230 |

| 2 | $15,510 | $19,380 | $17,850 |

| 3 | $xix,530 | $24,410 | $22,470 |

| 4 | $23,550 | $29,440 | $27,090 |

| 5 | $27,570 | $34,470 | $31,710 |

| 6 | $31,590 | $39,500 | $36,330 |

| vii | $35,610 | $44,530 | $40,950 |

| viii | $39,630 | $49,560 | $45,570 |

| Each additional person adds | $iv,020 | $5,030 | $iv,620 |

- In participating states, Medicaid eligibility is expanded; all individuals with income up to 133% of the poverty line qualify for coverage, including adults without dependent children.[31] [38] The law too provides for a 5% "income disregard", making the effective income eligibility limit 138% of the poverty line.[39] States may choose to increment the income eligibility limit beyond this minimum requirement.[39] Equally written, the ACA withheld all Medicaid funding from states failing to participate in the expansion. However, the Supreme Court ruled in National Federation of Independent Business 5. Sebelius (2012) that this withdrawal of funding was unconstitutionally coercive and that individual states had the right to opt out of the Medicaid expansion without losing pre-existing Medicaid funding from the federal authorities. For states that do expand Medicaid, the law provides that the federal government will pay for 100% of the expansion for the first three years, then gradually reduce its subsidy to 90% by 2020.[twoscore] [41] Equally of Apr 25, 2013,[update] 15 states—Alaska, Alabama, Georgia, Idaho, Indiana, Iowa, Louisiana, Mississippi, Nebraska, North Carolina, Oklahoma, Due south Carolina, Texas, Wisconsin, and Virginia—were non participating in the Medicaid expansion, with ten more—Kansas, Maine, Michigan, Montana, Missouri, Ohio, Pennsylvania, South Dakota, Utah, and Wyoming—leaning towards non participating.[42] [ needs update ]

- The Patient Protection and Affordable Care Human action eliminates lifetime and almanac limits from plans in the individual health benefits exchanges. This effectively eliminates the ceiling on fiscal risk for individuals in the individual exchanges.[43]

Subsidies [edit]

The subsidies for insurance premiums are given to individuals who buy a plan from an exchange and take a household income between 133% and 400% of the poverty line.[38] [44] [45] [46] Section 1401(36B) of PPACA explains that each subsidy will be provided equally an advanceable, refundable tax credit[47] and gives a formula for its adding:[48]

Except equally provided in clause (ii), the applicable percentage with respect to any taxpayer for any taxable year is equal to 2.eight percentage, increased by the number of percentage points (not greater than 7) which bears the same ratio to 7 percentage points equally the taxpayer's household income for the taxable year in excess of 100 percent of the poverty line for a family of the size involved, bears to an amount equal to 200 percent of the poverty line for a family of the size involved. *(ii) SPECIAL Dominion FOR TAXPAYERS Nether 133 PERCENT OF POVERTY LINE- If a taxpayer's household income for the taxable year is in excess of 100 percent, just not more 133 percent, of the poverty line for a family of the size involved, the taxpayer's applicative percentage shall be ii percent.

— Patient Protection and Affordable Care Act: Championship I: Subtitle E: Role I: Subpart A: Premium Calculation [48]

A refundable tax credit is a way to provide regime benefits to individuals who may accept no revenue enhancement liability[49] (such as the earned income taxation credit). The formula was changed in the amendments (Hr 4872) passed March 23, 2010, in section 1001. To qualify for the subsidy, the beneficiaries cannot be eligible for other acceptable coverage. The U.South. Department of Wellness and Homo Services (HHS) and Internal Revenue Service (IRS) on May 23, 2012, issued articulation final rules regarding implementation of the new state-based health insurance exchanges to comprehend how the exchanges will determine eligibility for uninsured individuals and employees of small businesses seeking to buy insurance on the exchanges, as well as how the exchanges will handle eligibility determinations for low-income individuals applying for newly expanded Medicaid benefits.[l] [51] Premium caps have been delayed for a twelvemonth on grouping plans, to give employers time to accommodate new accounting systems, just the caps are still planned to take effect on schedule for insurance plans on the exchanges;[52] [53] [54] [55] the HHS and the Congressional Research Service calculated what the income-based premium caps for a "silver" healthcare plan for a family unit of four would exist in 2014:

| Income | Premium | Additional Price-Sharing Subsidy | |||

|---|---|---|---|---|---|

| % of Federal poverty level | Dollars (2014)[a] | Cap (% of Income) | Max Out-of-Pocket | Avg Savings[b] | |

| 133% | $31,900 | 3% | $992 | $10,345 | $v,040 |

| 150% | $33,075 | iv% | $1,323 | $nine,918 | $five,040 |

| 200% | $44,100 | 6.3% | $2,778 | $8,366 | $4,000 |

| 250% | $55,125 | viii.05% | $4,438 | $half dozen,597 | $1,930 |

| 300% | $66,150 | ix.5% | $6,284 | $4,628 | $one,480 |

| 350% | $77,175 | 9.five% | $7,332 | $3,512 | $1,480 |

| 400% | $88,200 | nine.5% | $eight,379 | $two,395 | $ane,480 |

Notes

| |||||

Guaranteed issue [edit]

| State and district exchanges |

| Arkansas Wellness Connector |

| Covered California |

| Connect for Health Colorado |

| Access Wellness CT (Connecticut) |

| DC Health Link (District of Columbia) |

| Hawaiʻi Health Connector |

| Get Covered Idaho |

| Get Covered Illinois |

| Kynect (Kentucky) |

| Maryland Wellness Connection |

| Massachusetts Health Connector |

| MNsure (Minnesota) |

| Nevada Health Link |

| BeWellNM (New Mexico) |

| NY Land of Health (New York) |

| Embrace Oregon |

| Pennie (Pennsylvania) |

| HealthSource RI (Rhode Island) |

| Vermont Wellness Connect |

| Washington Healthplanfinder |

In the individual market, sometimes thought of as the "residuum market" of insurance,[ clarification needed ] insurers have generally used a process called underwriting to ensure that each individual paid for his or her actuarial value or to deny coverage altogether.[63] The House Committee on Energy and Commerce found that, betwixt 2007 and 2009, the four largest for-profit insurance companies refused insurance to 651,000 people for previous medical weather, a number that increased significantly each yr,[64] with a 49% increment in that time menses.[65] The same memorandum said that 212,800 claims had been refused payment due to pre-existing atmospheric condition and that insurance firms had business concern plans to limit money paid based on these pre-existing conditions. These persons who might not have received insurance under previous industry practices are guaranteed insurance coverage nether the ACA. Hence, the insurance exchanges volition shift a greater amount of financial take chances to the insurers, but will aid to share the cost of that risk among a larger pool of insured individuals. The ACA's prohibition on denying coverage for pre-existing conditions began on January 1, 2014. Previously, several state and federal programs, including most recently the ACA, provided funds for country-run high-take a chance pools for those with previously existing conditions.[66] [67] Several states have continued their high-gamble pools even later the kickoff marketplace enrollment period.[67]

Limit to toll variation [edit]

- Pricing Factors Allowed in the exchange under the ACA:[68]

-

- Age: 3:one

- Smoking status: one.5:one

-

Pricing variation will exist allowed by surface area (within a land) and family composition ("tier") as well.

Comparable tiers of plans [edit]

Within the exchanges, insurance plans are offered in four tiers designated from everyman premium to highest premium: bronze, silver, aureate, and platinum. The plans cover ranges from 60% to ninety% of bills in increments of x% for each programme. For those nether 30 (and those with a hardship exemption), a fifth "catastrophic" tier is as well available, with very loftier deductibles.[69]

Insurance companies select the doctors and hospitals that are "in-network".[ clarification needed ] [70]

Proponents of health care reform believe that allowing comparable plans to compete for consumer business in one convenient location will drive prices down. Having a centralized location increases consumer knowledge of the marketplace and allows for greater conformation to perfect competition. Each of these plans will also cap liabilities for consumers with out-of-pocket expenses at $half dozen,350 for individuals and $12,700 for families.[43]

2015 [edit]

A study by Avalere Wellness says that healthcare insurance premiums of popular plans available under Obamacare for 2015 rose by three-4% .[71]

According to the US Department of Wellness & Human Service, as enrollment for the Health Insurance Market began on November 15, about eleven.4 million people have explored their options, learned almost the financial assistance bachelor, and signed up for or renewed a health program that meets their needs and fits their budget. As of February, 2015, $268 was the average monthly tax credit for people who authorize for financial aid in 37 states using HealthcCare.gov through January xxx.[72]

2016 - [edit]

Economics of health insurance exchanges: the individual mandate [edit]

The health insurance advocacy grouping America'due south Health Insurance Plans was willing to accept these constraints on pricing, capping, and enrollment considering of the individual mandate: The individual mandate requires that all individuals buy health insurance.[73] [74] This requirement of the ACA allows insurers to spread the financial risk of newly insured people with pre-existing weather among a larger pool of individuals.

Additionally, a study done by Pauly and Herring estimates that individuals with pre-existing conditions in the 99th percentile of fiscal risk represented 3.95 times the average risk (hateful).[63] Figures from the House Committee on Energy and Commerce would indicate that approximately 1 million high-risk individuals will pursue insurance in the health benefits exchanges.[64] Congress has estimated that 22 million people will be newly insured in the health benefits exchanges.[75] Thus the high-adventure individuals do not number in loftier enough quantities to increase the net risk per person from previous practice. Information technology is thus theoretically profitable to accept the individual mandate in exchange for the requirements presented in the ACA.

Acronym [edit]

HIX (Health Insurance commutation) is emerging as the de facto acronym across country and federal authorities stakeholders, and the private sector technology and service providers that are helping states build their exchanges.[ citation needed ] The acronym HIX differentiates this topic from health information exchange, or HIE.[76]

The de facto acronym of HIX[77] will be replaced with HIEx in the tertiary Edition of the HIMSS Dictionary of Healthcare Data Engineering science Terms, Acronyms and Organizations, to exist released in March 2013.[update] [ commendation needed ]

Criticism and controversy [edit]

Get-go week of performance [edit]

The message, "Please try again later on", greeted many people who tried to view information on marketplace websites across the U.s.a. during the showtime week of operation. Websites were reported to have either crashed or to offering very sluggish response times. A argument past Todd Park, U.Southward. Master Technology Officer, resolved the initial disagreement about whether the culprit was the high volume of views or deeper technical issues[ citation needed ]: he asserted that glitches were caused by unexpected high volume at the federal health exchange (HealthCare.gov), when the site drew 250 m visitors instead of the 50-threescore one thousand expected, and claimed that the site would take worked with fewer visitors. More than than 8.1 million people visited the site from October 1–iv, 2013.[78]

On the date the Patient Protection and Affordable Care Human action of 2010 was enacted,[ when? ] only a few health insurance exchanges across the country were up and running. Amidst them were the Massachusetts Health Connector, the New York HealthPass - a non-profit exchange, and the Utah Health Substitution.[79] Advocates claim these exchanges brand these "markets" more efficient, providing oversight and structure, arguing that previous wellness insurance markets in the United States are poorly-organized and bargain with broad variations in coverages and requirements amongst different companies, employers, and policies.[80]

It was unknown how many people in total successfully enrolled in the get-go calendar week. The federal marketplace website was scheduled for maintenance on the weekend.[81] [82] Some reporters nicknamed the program "Slowbamacare".[83]

CGI Grouping came nether media scrutiny as a developer backside several marketplace websites,[84] afterward numerous bug[85] surfaced with the federal health insurance marketplace, HealthCare.gov.

On October 1, 2013, the state-run marketplaces also opened to the public, and some of them reported first statistics. During the starting time calendar week of enrollment:

- 28,699 people enrolled in the California wellness plan marketplace[83]

- 17,300 people enrolled in the Kentucky health plan market[83]

- More than 40,000 people enrolled in the NY State of Wellness marketplace[83]

- On October 8, 2013, The Seattle Times reported that more than than ix,400 people had enrolled in the Washington wellness plan marketplace.[83] However, a later report antiseptic that many included in that count were Medicaid enrollees. By October 21, 2013, simply four,500 Washington residents had enrolled in private insurance through the land market.[86]

Postponement of tax penalty [edit]

On Oct 23, 2013, The Washington Mail reported that Americans with no wellness insurance would have an boosted vi weeks earlier they would be penalized.[87] That deadline was extended to March 31, and those who do not enroll past then may still avoid incurring penalties and getting locked out of the healthcare enrollment organization this yr. Exemptions and extensions apply to:[88] [89]

- Those living in states that employ federal exchange, who may avail themselves of a "special entrollment period" that allows individuals to avoid penalties and enroll in a health programme by checking a blue box past mid-April 2014, stating they tried to enroll earlier the deadline (doing so provides a withal-undetermined amount of time to actually sign upward later that). The New York Mail reports: "This method volition rely on an award organisation; the government will non try to determine whether the person is telling the truth". State-run exchanges have their own rules; several will be granting similar extensions.[88] [89]

- Members of the Pre-Existing Condition Insurance Program, who were given a one-month extension until the stop of April 2014.[88] [89]

- Those who have successfully applied for exemption status based on criteria published by HealthCare.gov, who are not required to pay a tax penalization if they don't enroll in a wellness insurance programme.[90] [91]

Primary concerns [edit]

Medicaid expansion by state.[92] [93] [ needs update ]

Expanding Medicaid

Non expanding Medicaid

Still debating Medicaid expansion

- Exclusion of many lower-income individuals

- NPR reported that large numbers of low income people were excluded in states that did not offering Medicaid expansion to 133% of the poverty line.[94] [95]

- Information security

- Minnesota's healthcare exchange was reported to have accidentally e-mailed personal information of more than 2,400 insurance agents to an insurance broker, according to the Minnesota Star Tribune.[96]

- Loss of grouping coverage for part-time employees

- According to NPR, some employers such as Trader Joe'southward and Home Depot accept decided to end health insurance for their part-time workers.[97]

- Scams

- Scams were expected because of confusion over enrollment.[98] [99]

- Restricted and narrow networks

- Some exchanges have been criticized for offering health plans that necessitate too many out-of-network claims. On October 5, 2013, Seattle Children's hospital filed a lawsuit for "failure to ensure adequate network coverage" when merely ii insurers included Children's in their marketplace plan.[100]

- Concerns have likewise been raised well-nigh insurance carriers' efforts to limit the number of providers in their networks to reduce costs. A study of the California marketplace confirmed these concerns, but also showed that geographic admission was similar and quality at times superior in marketplace-based plans.[101]

- "Cherry-picking"

- The individual health insurance industry fears that restricted eligibility and a market size that is too small could issue in higher premiums, encourage "reddish-picking" of customers by insurers, and force a clearance of the exchange. That is what some believe volition happen in Texas and California in their failed exchanges.[102] One of these factors, "cherry-picking" of customers, will not be possible in the country-run exchanges mandated by the ACA, because all insurance plans volition be "guaranteed issue" in 2014. Furthermore, the law will bring millions of new enrollees into the market place by way of the individual mandate requirement for all citizens to buy health insurance and increment marketplace size.[103]

Congressional reaction [edit]

On October 28 and 29, 2013, Sen. Lamar Alexander (R-TN) and Rep. Lee Terry (R, NE-2) introduced the Exchange Data Disclosure Human action (S. 1590 and H.R. 3362, respectively).[104] [105] Terry's bill would have required the United states of america Section of Health and Human Services to submit weekly reports to Congress on the status of HealthCare.gov including "…weekly updates on the number of unique website visitors, new accounts, and new enrollments in a qualified wellness plan, besides as the level of coverage," separating the information by state, as well as reports on efforts to fix the cleaved portions of the website.[106] The reports would have been due every Monday until March 31, 2015, and would have been available to the public.[107]

On January 16, 2014, Terry's bill passed the House of Representatives; 226 Republicans and 33 Democrats voted yes.[108] Alexander'due south nib died in committee.[104]

Country-Based Marketplaces [edit]

A State-based Marketplace (SBM) is a state-specific online marketplace where American citizens and legal residents can comparing shop, utilise, and enroll in subsidized wellness insurance plans via a government agency. Similar to Healthcare.gov, but created and maintained by the private land. Sometimes referred to equally a State-based Exchange (SBE),[109] State-based marketplaces strive to limit consumer confusion by standardizing information on plan benefits and making it easier to compare insurance policy cost and quality.

States that have opted to implement a State-based Marketplace are required to offering numerous forms of assistance to consumers searching for coverage, such as toll-free hotlines to help consumers with plan pick, assistance in determining eligibility for federal subsidies or Medicaid, and conducting outreach to educate consumers on available coverage options in their state.

States with Country-based Marketplaces [edit]

Country-based Marketplaces accept developed as technology matures and the market and individual land needs have changed. Numerous states have opted to implement their own SBM.

This includes:

- California – Covered California[110]

- Colorado – Connect for Health Colorado[111]

- Connecticut – Admission Wellness CT[112]

- Commune of Columbia – DC Wellness Link[113]

- Idaho – Your Wellness Idaho[114]

- Maryland – Maryland Health Connection[115]

- Massachusetts – Health Connector[116]

- Minnesota – MNsure[117]

- New Jersey – Get Covered NJ[118]

- New York – New York State of Health[119]

- Pennsylvania – Pennie(tm)[120]

- Rhode Island – HealthSource RI[121]

- Vermont – Vermont Health Connect[122]

- Washington – Washington Healthplanfinder[123] [124]

Cover Oregon website failure [edit]

In March 2015, Oregon officially abolished its state-run health insurance marketplace, "Cover Oregon", in favor of a federally-run commutation.[125]

Private health insurance exchanges [edit]

A private health insurance exchange is an exchange run past a private sector company or nonprofit. Wellness plans and insurance carriers in a individual substitution must meet certain criteria defined past the commutation management. Private exchanges combine applied science and human being advocacy, and include online eligibility verification and mechanisms for allowing employers who connect their employees or retirees with exchanges to offer subsidies. They are designed to help consumers find plans personalized to their specific health conditions, preferred doctor/hospital networks, and budget. These exchanges are sometimes called marketplaces or intermediaries, and work directly with insurance carriers, effectively acting every bit extensions of the carrier.[ citation needed ] The largest and most successful[ peacock term ] private health care commutation is CaliforniaChoice, established past Choice Administrators in 1996.[126]

Private health exchanges predate the Affordable Intendance Deed. One instance of an early health care exchange is International Medical Substitution (IMX), a company venture financed in Louisville, Kentucky, by Standard Telephones and Cables, a big British applied science company (now Nortel), to develop the exchange concept in the U.S. using on-line engineering. The product was created in the mid-1980s. IMX developed an eligibility verification system, a claims management system, and a bank-based payments administration system that would manage payments between the patient, the employer, and the insurance carrier. Like proposed exchanges today, it focused on standards of care, utilization review by a tertiary political party, individual insurer participation, and cost reduction for the wellness care system through product simplification. The focus was on creating local or regional exchanges that offered a series of standardized wellness care plans that reduced the complication and price of acquiring or agreement wellness intendance insurance, while simplifying claims administration. The organisation was modeled after the standardized stock exchange and banking industry back office processes. The major difference was that IMX health care exchanges would provide their products through a national network of existing commercial banks rather than setting up a duplicate payment and administration systems network as proposed today. The IMX product rights were caused by Canticle (then Blue Cross and Blue Shield of Kentucky). The exchange product became the basis for inter-carrier claims settlement between commercial insurance carriers and Bluish Cross organizations. The founders of IMX were from height management at Humana, and top direction of Kickoff Tennessee National Corp (at present First Horizon).

In overlapping markets, the co-being of public and individual commutation plans can lead to confusion when speaking of an "exchange plan." In California, Anthem Blue Cross offers HMO plans through both the state-run Covered California exchange and the private CaliforniaChoice exchange, but physician networks are non identical. Physicians advertizement acceptance of Anthem Blueish Cross Substitution HMOs may misinform individuals enrolled in Anthem Blue Cross Exchange HMOs through the private exchange.

Meet likewise [edit]

- Health care reform in the United States

- Health organization

- Universal wellness coverage past country

References [edit]

- ^ "What is the Wellness Insurance Marketplace?". Healthcare.gov. U.S. Centers for Medicare & Medicaid Services.

- ^ Lewis, Nicole (July 12, 2011). "HHS Proposes Health Insurance Substitution Rules". InformationWeek: Healthcare. UBM TechWeb. Archived from the original on July 14, 2011.

- ^ a b Mangan, Dan (May 1, 2014). "Latest score: Obamacare enrolls 8.02 one thousand thousand past April xix". CNBC.

- ^ Alonso-Zaldivar, Ricardo (November ix, 2014). "Higher bar for wellness law in 2nd sign-upwards season". CBS Money Watch. CBS Interactive. Archived from the original on November ten, 2014.

- ^ "Market Enrollment, 2014-2020". The Henry J. Kaiser Family Foundation. 2020-04-07. Retrieved 2020-04-xiv .

- ^ Carrns, Ann (June fourteen, 2014). "Private Health Intendance Exchanges enroll more Predicted". New York Times (New York ed.). p. B6. Retrieved 16 July 2014.

- ^ Scholl, Martin (Oct sixteen, 2014). "Take advantage of the emerging market identify of the Health Benefit Exchanges". HIPAA Suite. Archived from the original on Nov 24, 2014.

- ^ "Land Decisions For Creating Health Insurance Exchanges, equally of May 28, 2013 - Table". Kaiser Family Foundation. May 28, 2013.

- ^ "Country Decisions For Creating Health Insurance Exchanges, as of May 28, 2013 - Map". Kaiser Family Foundation. May 28, 2013.

- ^ Hass, Christopher (June 3, 2009). "President Obama Reiterates Support for Public Option and Health Insurance Exchange". Obama for America. Archived from the original on August xx, 2012. Retrieved February 7, 2014.

- ^ a b Grier, Peter (March ten, 2010). "Wellness care reform nib 101: What'southward a health 'exchange'?". Christian Science Monitor.

- ^ "Welcome to the Marketplace". Healthcare.gov.

- ^ "What is the Health Insurance Marketplace?". Healthcare.gov.

- ^ Luhby, Tami (April 23, 2013). "Millions eligible for Obamacare subsidies, but virtually don't know it". CNN.

- ^ "Establishing Wellness Insurance Marketplaces: An Overview of State Efforts". Kaiser Family unit Foundation. May two, 2013.

- ^ "How can I get ready to enroll in the Market place?". Healthcare.gov. Archived from the original on June 26, 2013.

- ^ Morgan, David; Begley, Sharon (September 30, 2013). "Obamacare push accelerates as government shutdown nears". Reuters. Retrieved Oct 1, 2013.

Sebelius said on Mon that 'the cardinal engagement really is the 15th of December,' the borderline for ownership coverage that starts on January 1.

- ^ "Glossary: Open Enrollment Menstruation". Healthcare.gov. Retrieved Oct iv, 2013.

- ^ Young, Jeffrey (September 25, 2013). "Obamacare Benefits Enrollment Will Start Slowly, White House Predicts". The Huffington Post . Retrieved October 2, 2013.

- ^ Cohn, Jonathan (August five, 2013). "Burn down Your Obamacare Card, Burn down Yourself". The New Republic.

- ^ Goldstein, Amy (2010). "Priority One: Expanding Coverage". In The Staff of the Washington Mail service (ed.). Landmark: The Inside Story of America'due south New Health-Care Constabulary and What It Means for United states All. New York: Public Diplomacy. pp. 73–83. ISBN9781410428998.

- ^ a b "Open Enrollment Outreach and Education Round-Upward". HHS.gov/HealthCare. U.S. Section of Health & Man Services. December fifteen, 2014. Archived from the original on January 4, 2015.

- ^ Acosta, Jim; Cohen, Tom (December 31, 2013). "More than than 2 meg enrolled under Obamacare". CNN.

- ^ content

- ^ "I take been denied coverage because I accept a pre-existing condition. What will this law do for me?" (PDF). Health Care Reform Often Asked Questions. New Hampshire Insurance Department. p. ii. Retrieved June 28, 2012.

- ^ Binckes, Jeremy; Wing, Nick (March 22, 2010). "The Top xviii Immediate Effects Of The Health Care Bill". The Huffington Post . Retrieved March 22, 2010.

- ^ "What does Marketplace health insurance cover?". Healthcare.gov.

- ^ "Minimum Coverage Provision". American Public Health Association. Archived from the original on 2014-07-01. Retrieved 2013-x-02 .

- ^ a b "Technical Explanation of The Revenue Provisions of the Reconciliation Act of 2010, as Amended, in Combination With the Patient Protection And Affordable Care Human activity". Joint Committee on Taxation. March 21, 2010.

Generally, in 2010, the filing threshold is $9,350 for a single person or a married person filing separately and is $18,700 for married filing jointly.

- ^ Doyle, Brion B. (March 5, 2013). "Agreement the Impacts of the Patient Protection and Affordable Intendance Human action". The National Law Review . Retrieved 17 Apr 2013.

- ^ a b Galewitz, Phil (March 26, 2010). "Consumers Guide To Wellness Reform". Kaiser Health News.

- ^ Downey, Jamie (March 24, 2010). "Tax implications of wellness care reform legislation". The Boston World . Retrieved March 25, 2010.

- ^ Luhby, Tami (August 13, 2013). "Uninsured next twelvemonth? Hither's your Obamacare penalisation". CNN.

- ^ Kliff, Sarah; Klein, Ezra (March 27, 2012). "Individual mandate 101: What it is, why information technology matters". Wonkblog at the Washington Postal service. Retrieved July 2, 2012.

- ^ "Requirement to maintain minimum essential coverage". Cornell University Law School Legal Information Institute. September eighteen, 2013.

Described in 26 USC § 5000A(f)(iv)(A)

- ^ Sahadi, Jeanne (June 29, 2012). "How wellness insurance mandate will work". CNN. Retrieved July 12, 2013.

- ^ "2013 Poverty Guidelines". United states Department of Health and Human Services.

- ^ a b Rice, Sabriya (March 25, 2010). "5 key things to retrieve about health care reform". CNN. Retrieved May 21, 2010.

- ^ a b "Medicaid Expansion: 5. Is Medicaid eligibility expanding to 133 or 138 percent FPL, and what is MAGI?". American Public Health Clan.

- ^ Luhby, Tami (July i, 2013). "States forgo billions by opting out of Medicaid expansion". CNN.

- ^ "Is Medicaid Expansion Good for the States?". U.S. News & World Written report.

- ^ Kliff, Sarah (April 25, 2013). "The outlook for Medicaid expansion looks bleak". Washingtonpost.com . Retrieved July 17, 2013.

- ^ a b MacGillis, Alec (2010). "The Insurers: More than Customers, More than Restrictions". In The Staff of the Washington Mail (ed.). Landmark: The Inside Story of America'due south New Health-Care Law and What It Means for Us All. New York: Public Affairs. pp. 93–98. ISBN9781410428998.

- ^ Peterson, Chris L.; Gabe, Thomas (April six, 2010). "Health Insurance Premium Credits Nether PPACA (P.L. 111-148)" (PDF). Congressional Research Service.

- ^ Galewitz, Phil (March 22, 2010). "Wellness reform and you: A new guide". msnbc.com. Archived from the original on March 25, 2010. Retrieved March 23, 2010.

- ^ Grier, Peter (March 20, 2010). "Health intendance reform beak 101: Who gets subsidized insurance?". The Christian Science Monitor.

- ^ wikisource:Patient Protection and Affordable Care Act/Title I/Subtitle E/Part I/Subpart A

- ^ a b Patient Protection and Affordable Care Human action: Championship I: Subtitle E: Part I: Subpart A: Premium Calculation

- ^ "Refundable Tax Credits". Breadstuff for the Earth Institute. Archived from the original on March 5, 2012.

- ^ "Health Insurance Premium Taxation Credit" (PDF). Federal Register. Washington, D.C.: Government Press Part. 77 (100): 30377–30400. May 23, 2012.

- ^ a b "Treasury Lays the Foundation to Deliver Revenue enhancement Credits to Help Make Health Insurance Affordable for Heart-Class Americans" (PDF) (Press release). United States Department of the Treasury. August 12, 2011.

- ^ Pear, Robert (August 12, 2013). "A Limit on Consumer Costs Is Delayed in Health Intendance Law". The New York Times.

- ^ Cohn, Jonathan (August thirteen, 2013). "The Latest Right-Wing Freakout Over Obamacare". The New Commonwealth.

- ^ Goddard, Teagan (August xiii, 2013). "Just Another Obamacare Filibuster". Roll Phone call. Archived from the original on September 27, 2013. Retrieved Oct 2, 2013.

- ^ Chait, Jonathan (Baronial 15, 2013). "George Will: Now Obama Is Worse Than Nixon". New York.

- ^ a b c "Private Wellness Insurance Provisions in PPACA (P.L. 111-148)" (PDF). Congressional Research Service. April fifteen, 2010. Archived from the original (PDF) on December 12, 2012. Retrieved October 2, 2013.

- ^ a b "Health Insurance Premiums: By High Costs Volition Become the Present and Futurity Without Health Reform" (PDF). HealthCare.gov. January 28, 2011. Archived from the original (PDF) on January fifteen, 2013.

- ^ "Financing Center of Excellence | SAMHSA | Health Insurance Premiums: Past High Costs Will Get the Nowadays and Future Without Health Reform". Substance Abuse and Mental Health Services Administration. March fourteen, 2011. Archived from the original on September 21, 2012. Retrieved June 29, 2012.

- ^ "Health Insurance Premium Credits Under PPACA" (PDF). Congressional Research Service. April 28, 2010. Archived from the original (PDF) on Oct 27, 2010.

- ^ "An Analysis of Health Insurance Premiums Under the Patient Protection and Affordable Intendance Act". Congressional Budget Office. November thirty, 2009.

- ^ "Policies to Improve Affordability and Accountability". whitehouse.gov. Archived from the original on 2017-02-08 – via National Archives.

- ^ "Subsidy Calculator: Premium Assist for Coverage in Exchanges". Kaiser Family Foundation.

- ^ a b Pauly, Mark 5.; Herring, Bradley (May 2007). "Risk Pooling and Regulation: Policy and Reality in Today's Private Health Insurance Market place". Health Affairs. 26 (3): 770–779. doi:10.1377/hlthaff.26.iii.770. PMID 17485756.

- ^ a b Waxman, Henry A.; Stupak, Bart (October 12, 2012). "Re: Coverage Denials for Pre-Existing Atmospheric condition in the Private Health Insurance Market [Memorandum]" (PDF). United States Firm Committee on Energy and Commerce. Retrieved Dec xv, 2012.

- ^ Hall, Jean P. (October 19, 2010). "Affordable Care Human activity Options for People with Preexisting Conditions". The Commonwealth Fund.

- ^ Vesely, Rebecca (February 28, 2011). "States endeavour it again". Modern Healthcare. 41 (9): 17.

- ^ a b Haeder, Simon (2013). "Making the Affordable Care Deed Work: Loftier-Risk Pools and Health Insurance Marketplaces". The Forum. 11 (3). doi:10.1515/for-2013-0056. S2CID 147178678.

- ^ "Compilation of Patient Protection and Affordable Care Deed" (PDF). Part of the Legislative Counsel. June 9, 2010.

- ^ "How do I choose Marketplace insurance?". HealthCare.gov. Retrieved Oct 28, 2013.

There are five categories of Marketplace insurance plans: Bronze, Argent, Gold, Platinum, and Catastrophic.

- ^ Somashekhar, Sandhya; Kliff, Sarah (September 24, 2013). "Premiums unveiled show wide range for health overhaul plans". The Seattle Times. Archived from the original on December eighteen, 2014.

- ^ Tergesen, Anne. "Obamacare premiums for 2015 include some big changes".

- ^ "By the Numbers: Open Enrollment for Health Insurance". HHS.gov/HealthCare. U.S. Department of Health & Human Services. February 13, 2015. Archived from the original on February fifteen, 2015.

- ^ Japsen, Bruce (June 17, 2012). "Mandate To Purchase Coverage: Health Insurance Manufacture's Idea, Not Obama'south". Forbes . Retrieved February seven, 2014.

- ^ "Individual Responsibility - Glossary". HealthCare.gov. Archived from the original on June nineteen, 2013. Retrieved 3 June 2013.

- ^ Board, Editorial (February 7, 2014). "The CBO report does not show the new health-care police force is declining". The Washington Mail.

- ^ Dimick, Chris (June 1, 2010). "Accrediting HIEs". Journal of AHIMA.

- ^ See more data on the HIMSS Dictionary at second Edition of the HIMSS Dictionary of Healthcare Information Technology Terms, Acronyms and Organizations.

- ^ Mullaney, Tim (October half-dozen, 2013). "Obama adviser: Demand overwhelmed HealthCare.gov". United states of america Today.

- ^ "The state of your health insurance market". healthinsurance.org.

- ^ Blumberg, Linda J.; Pollitz, Karen (April 1, 2009). "Health Insurance Exchanges: Organizing Health Insurance Marketplaces to Promote Health Reform Goals". Urban Institute.

- ^ Lohr, Kathy (October 5, 2013). "Glitches Slow Health Exchange Sign-ups". NPR.

- ^ Goldstein, Amy; Sun, Lena H.; Somashekhar, Sandhya (October 1, 2013). "Blitz of interest continues on insurance Spider web sites". The Washington Post.

- ^ a b c d e Westneat, Danny (October viii, 2013). "Obamacare is here, GOP, fix or not". The Seattle Times.

- ^ Auerbach, David (October viii, 2013). "What actually went wrong with healthcare.gov?". Slate. Retrieved February 7, 2014.

- ^ Periroth, Nicole (October 2, 2013). "Bug at Wellness Care Web Site Non From Online Assail, Experts Say". New York Times.

- ^ Landa, Amy Snowfall (Oct 21, 2013). "Washington Healthplanfinder: more than 35,000 have enrolled in 3 weeks". The Seattle Times.

- ^ Somashekhar, Sandhya; Goldstein, Amy; Eilperin, Juliet (October 23, 2013). "Americans will have an extra six weeks to buy health coverage before facing penalty". The Washington Mail.

- ^ a b c SARA MORRISON (March 25, 2014). "Obamacare: Enrollees Get Post-Borderline 'Special Enrollment Period' Extension".

- ^ a b c "Obama Administration Announces Health Care Extension". Fox News. March 25, 2014.

- ^ DAN RITTER (March 25, 2014). "I'll Have the Revenue enhancement: ten Obamacare Exemptions You Don't Want". Wall Street Cheat Canvas.

- ^ "How do I qualify for an exemption from the fee for not having health coverage?". HealthCare.gov . Retrieved March 26, 2014.

- ^ "Status of State Activeness on the Medicaid Expansion Decision, every bit of July ane, 2013 - Table". Kaiser Family unit Foundation. June 20, 2013.

- ^ "Status of State Activeness on the Medicaid Expansion Decision, as of July 1, 2013 - Map". Kaiser Family Foundation. June 20, 2013.

- ^ Allen, Greg (October 1, 2013). "In Florida, Insurer And Nonprofits Work On Enrollment". NPR.

- ^ "Subsidy Calculator". Kaiser Family Foundation.

- ^ Condon, Stephanie (October ii, 2013). "Obamacare marketplaces raise data security concerns". CBS.

- ^ Ydstie, John (Oct iv, 2013). "Part-Time Workers Search New Exchanges For Health Insurance". NPR.

- ^ Thompson, Connie (September 30, 2013). "Scammers newest ruse: Health care reform". KLEW-Goggle box.

- ^ Tarpley, Tiffany (October i, 2013). "Protecting yourself from healthcare police scams". WDJT-Idiot box.

- ^ Landa, Amy Snow (October 4, 2013). "Left off many networks, Seattle Children'southward sues". The Seattle Times.

- ^ Haeder, Simon; Weimer, David; Mukamel, Dana (2015). "California Infirmary Networks Are Narrower In Marketplace Than In Commercial Plans, Just Access And Quality Are Like" (PDF). Wellness Diplomacy. 34 (5): 741–748. doi:10.1377/hlthaff.2014.1406. PMID 25941274.

- ^ McGarr, Cappy (October 5, 2009). "A Texas-Sized Health Intendance Failure". The New York Times . Retrieved October half dozen, 2009.

- ^ "The Affordable Care Act: The Individual Mandate" (PDF). University of Missouri. Retrieved February 23, 2014.

- ^ a b "Southward.1590 - Exchange Data Disclosure Act: Actions Overview". Congress.gov. Library of Congress. Retrieved February 17, 2017.

- ^ "H.R. 3362 - All Actions". United States Congress. Retrieved January vii, 2014.

- ^ Kasperowicz, Pete (January 4, 2014). "House GOP to demand O-Care updates". The Hill . Retrieved Jan 7, 2014.

- ^ "Text of H.R. 3362". GovTrack. Retrieved Jan seven, 2014.

- ^ "H.R. 3362 (113th): Exchange Data Disclosure Human action — House Vote #23". GovTrack. Civic Impluse, LLC. January sixteen, 2014.

- ^ "Country-based Exchanges | CMS". www.cms.gov . Retrieved 2021-05-24 .

- ^ "Covered California™ | The Official Site of California'southward Health Insurance Marketplace". world wide web.coveredca.com . Retrieved 2021-05-25 .

- ^ "Connect for Health Colorado". Connect for Health Colorado . Retrieved 2021-05-25 .

- ^ "Access Director for Web Login". world wide web.accesshealthct.com . Retrieved 2021-05-25 .

- ^ "DC Health Link | Welcome to DC'south Wellness Insurance Marketplace". dchealthlink.com . Retrieved 2021-05-25 .

- ^ "Your Wellness Idaho » Idaho's Official Health Insurance Marketplace". world wide web.yourhealthidaho.org . Retrieved 2021-05-25 .

- ^ "Home". Maryland Health Connection . Retrieved 2021-05-25 .

- ^ "Acquire". Massachusetts Health Connector . Retrieved 2021-05-25 .

- ^ "MNsure Domicile". MNsure . Retrieved 2021-05-25 .

- ^ "GetCoveredNJ". www.nj.gov . Retrieved 2021-05-25 .

- ^ "NY Land of Health, The Official Health Plan Marketplace". nystateofhealth.ny.gov . Retrieved 2021-05-25 .

- ^ "Pennie". Retrieved 2021-05-25 .

- ^ "Oft Asked Questions". HealthSource RI . Retrieved 2021-05-25 .

- ^ "VHC Landing Folio". portal.healthconnect.vermont.gov . Retrieved 2021-05-25 .

- ^ "Dwelling house | Washington Healthplanfinder". www.wahealthplanfinder.org . Retrieved 2021-05-25 .

- ^ GetInsured. "Which States Have State-Based Marketplaces?". GetInsured . Retrieved 2021-05-25 .

- ^ Manning, Jeff (Apr 25, 2014). "Cover Oregon: $248 million state exchange to be jettisoned in favor of federal organisation". The Oregonian . Retrieved April 27, 2014.

- ^ "About Us". CaliforniaChoice . Retrieved September 13, 2017.

External links [edit]

- HealthCare.gov

- Status of Federal Funding for State Implementation of Health Insurance Exchanges Congressional Research Service

- C-Span Video Library: Search Health Insurance Exchange

- Come across "Clips" tab then "Clips Timeline" drop-down for abstracts of edited clips from the following videos:

- Wellness Care Law Exchanges Apr 22, 2013, Jenny Gilded, Kaiser Health News correspondent, Interview

- Study Video Issue Health Insurance Exchanges Jul 25, 2013, Politico Pro Wellness Care Breakfast Briefing

- Update on the Health Care Police force Jul one, 2013, Julie Rovner, National Public Radio health policy correspondent, Interview

- Overview of Health Insurance Exchanges, Congressional Research Service, July one, 2016

Source: https://en.wikipedia.org/wiki/Health_insurance_marketplace

0 Response to "Removing a Family Member on Health Insurance Marketplace"

Post a Comment